The U.S. Got Over 3,000 New Fast Charging Plugs In Q1 2026, Uptime Increasing

The U.S. market for new electric vehicles is not experiencing strong growth at the moment, but that has not slowed the pace of expansion among EV charging providers. Companies across the sector continue to build out infrastructure, maintaining momentum despite softer vehicle sales.

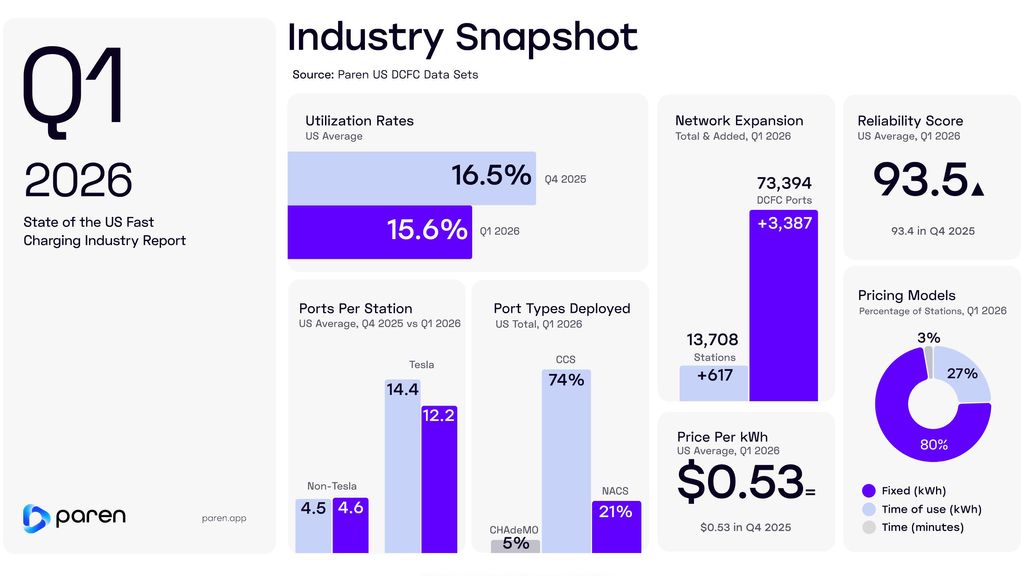

In the first quarter alone, more than 3,000 new DC fast charging plugs were added nationwide, based on data from Paren, a platform that monitors over 95% of the country’s fast-charging network in real time. From January through March, operators deployed 3,387 new ports and brought 617 new stations online. This pushed the national total to 13,708 stations and 73,394 ports. The pace of growth closely mirrors the first quarter of last year, when 3,331 ports were installed, indicating that expansion has remained consistent year over year. Utilization rates have also held steady, signaling that demand continues to absorb the added capacity.

At the same time, the strategy behind network expansion is shifting in 2026. Rather than focusing primarily on building entirely new sites, charging companies are increasingly concentrating on expanding existing locations by adding more stalls. This approach allows operators to scale capacity more efficiently at proven sites. In parallel, most new installations are high-power chargers, with the majority delivering more than 250 kilowatts, reflecting a broader move toward faster charging performance.

Reliability is also improving as operators incorporate lessons from earlier deployments. Average uptime across networks has increased to between 90% and 95%, compared to a range of roughly 85% to 92% last year. Pricing, meanwhile, has remained relatively stable, with most stations charging between $0.45 and $0.55 per kilowatt-hour, even as fuel prices remain elevated and continue to draw attention to charging costs.

Tesla remains the largest player in the U.S. DC fast charging market, though its share of new installations has declined. The company added 880 ports in the first quarter, representing 26% of total deployments, down from levels exceeding 40% in prior periods. Other operators are expanding their presence, with Ionna installing 278 ports and Red E adding 264.

Connector preferences continue to be led by CCS1, while Tesla’s NACS standard is gaining traction. During the quarter, non-Tesla networks deployed 2,102 CCS1 connectors alongside 606 NACS ports. Meanwhile, 154 CHAdeMO ports were added, a legacy standard once used by earlier models such as the Nissan Leaf but now largely phased out. Despite this shift, non-Tesla sites still maintain more CHAdeMO connectors than NACS, even as vehicles equipped with NACS continue to increase in number.

EV sales declined by 27% in the first quarter compared to the same period last year, yet charging companies are continuing to invest. Infrastructure projects often require long planning and construction timelines, limiting the ability to adjust quickly to short-term market fluctuations. At the same time, there remains a clear need to support the growing number of EVs already in operation, as well as those entering the market. Over the longer term, operators are positioning themselves for inevitable renewed growth in EV adoption by ensuring charging capacity is in place ahead of demand.

EVinfo.net’s Take: U.S. EV Charging Will Keep Growing, Especially During the Current EV Sales Boom From High Wartime Fuel Prices

High fuel prices are once again reshaping the transportation landscape in the United States, and this time the impact is accelerating a structural shift rather than creating a temporary spike in behavior. As gasoline costs climb amid ongoing geopolitical instability, electric vehicles are becoming not just an environmental choice, but a practical financial decision. That shift is driving a parallel surge in demand for EV charging infrastructure, and the growth trajectory is unlikely to slow.

For consumers, the math is increasingly straightforward. Volatile fuel prices translate into unpredictable monthly expenses, while electricity offers far more stability. Home charging, in particular, gives drivers a level of cost control that internal combustion vehicles simply cannot match. As more households run those numbers, EV adoption rises, and with it, the need for accessible, reliable charging beyond the home.

This dynamic is already visible in the data. Periods of elevated fuel prices consistently correlate with spikes in EV interest and sales. What makes the current moment different is scale. The U.S. EV market is no longer in its early adopter phase. It is entering a broader adoption curve, where infrastructure availability becomes a decisive factor in sustaining momentum.

Charging deployment is responding accordingly. Utilities, private networks, retailers, and fleet operators are all expanding their footprints. Fast charging corridors are becoming denser along major highways, while Level 2 charging continues to proliferate in workplaces, multifamily housing, and commercial destinations. This diversification is critical. A mature EV ecosystem depends on a mix of charging speeds and locations that align with real-world driving patterns.

Importantly, investment is no longer driven solely by policy mandates or sustainability goals. It is increasingly supported by clear economic signals. Charging stations generate recurring revenue, attract customers to physical locations, and enhance property value. For businesses, hosting chargers is evolving from a branding exercise into a measurable return-on-investment decision.

At the same time, technology improvements are addressing long-standing concerns. Faster charging speeds, better software integration, and more reliable hardware are improving the user experience. As uptime and performance become central to network competitiveness, operators are focusing more on maintenance, data analytics, and energy management.

There are still challenges. Grid capacity, permitting timelines, and fragmented ownership structures can slow deployment. Reliability remains uneven across networks, and consumer confidence depends heavily on consistent performance. However, these are execution issues, not demand issues. The underlying market signal is strong and getting stronger.

High fuel prices are acting as an accelerant, not the root cause. The transition to electric transportation has been building for years, supported by falling battery costs, expanding model availability, and growing consumer awareness. What the current environment does is compress timelines. It pushes more consumers and businesses to act now rather than later.

As a result, U.S. EV charging infrastructure will continue to scale rapidly. The combination of economic pressure, technological progress, and increasing adoption creates a reinforcing cycle. More EVs drive more charging demand, which drives more investment, which in turn supports further adoption.

In that context, the question is no longer whether EV charging will grow. It is how quickly stakeholders can build, operate, and maintain the infrastructure needed to support a market that is moving faster than many anticipated.

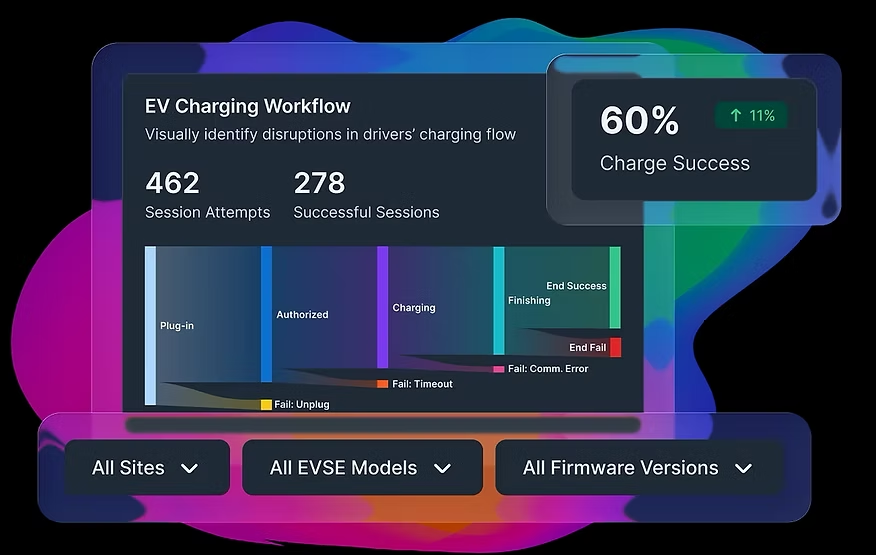

Clockwork: The Reliability Layer for EV Charging Networks

EV charging reliability remains a problem, and Clockwork has great solutions for customers in the U.S. and Canada. See Paren’s report for the current status of the Canadian EV charging market: Canadian EV Fast Charging — Q1 2026.

Clockwork Energy focuses on building and operating energy infrastructure that supports electrification at scale. The company works at the intersection of power, transportation, and real estate, helping clients deploy systems that are reliable, efficient, and built for long-term performance.

At its core, Clockwork delivers end-to-end energy solutions. This includes project development, engineering, financing, construction, and ongoing operations. Rather than treating these as separate phases, the company integrates them into a single workflow, reducing complexity and improving execution across the lifecycle of a project.

A major focus is electric vehicle charging infrastructure. Clockwork partners with property owners, fleets, and businesses to design and deploy charging systems tailored to site-specific needs. This includes everything from power assessments and utility coordination to equipment selection and software integration. The goal is not just installation, but creating infrastructure that performs consistently and scales with demand.

The company also works with distributed energy resources such as solar and battery storage. By combining these technologies with EV charging, Clockwork helps optimize energy usage, reduce operating costs, and improve resilience. These integrated systems are designed to respond to real-world conditions, including fluctuating energy prices and grid constraints.

Financing and ownership structures are another key component. Clockwork offers flexible models that allow clients to deploy infrastructure without taking on unnecessary capital burden. This approach enables faster adoption while aligning incentives around long-term system performance.

Once systems are deployed, Clockwork remains involved through monitoring, maintenance, and optimization. Performance data is used to improve uptime, manage energy consumption, and ensure that assets deliver consistent value over time.

Ultimately, Clockwork Energy positions itself as a long-term partner in electrification, focused on turning complex energy challenges into streamlined, scalable solutions.

At ACT Expo, May 4-7, Las Vegas, DON’T MISS:

Meetings:

EVSTAR’s Ted Manser and Hubert Kim.

TEAL team and Robb Monkman, CMO.

Booths:

Ampcontrol: Booth 2327

Autel Energy: Booth 3711

Camber Charging: Booth 2431