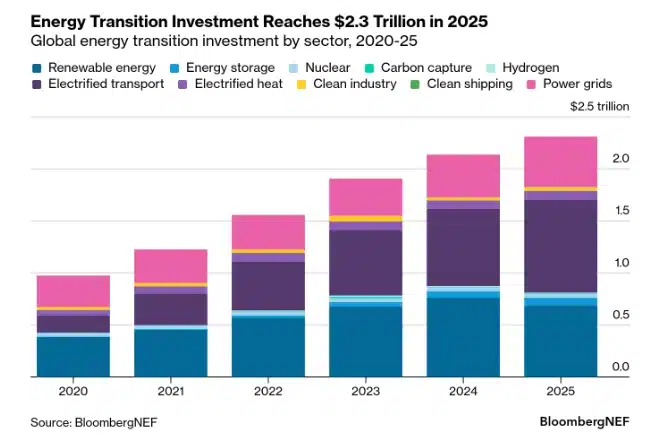

Global Energy Transition Investment Reached Record $2.3 Trillion in 2025, Up 8% from 2024

On January 26, 2026, BloombergNEF’s report Energy Transition Investment Trends showed some encouraging findings. The report finds that global investment in the energy transition reached a record $2.3 trillion in 2025, an 8% increase from the previous year. The largest drivers were electrified transport at $893 billion, renewable energy at $690 billion, and grid investment at $483 billion. Renewable energy investment declined 9.5% year over year as changes to power market regulations in China introduced new uncertainty. All other sectors tracked by BNEF recorded higher investment levels, with the exception of hydrogen, which totaled $7.3 billion, and nuclear, which reached $36 billion.

The report shows that clean energy supply investment outpaced fossil fuel supply investment for the second consecutive year, with the gap widening to $102 billion from $85 billion in 2024. Clean energy investment, including renewables, nuclear, carbon capture, hydrogen, energy storage and power grids, continued to grow, while fossil fuel supply investment declined for the first time since 2020, falling by $9 billion year over year. The decrease was driven primarily by reduced upstream oil and gas spending and a $14 billion drop in fossil power generation investment, partially offset by higher spending on gas and coal. Despite reaching an all-time high, growth in overall energy transition investment has slowed steadily, from 27% in 2021 to 8% in 2025.

Asia Pacific remained the largest investment region, accounting for 47% of the global total in 2025. China led overall investment at $800 billion but posted its first decline in renewable funding since 2013. India’s investment increased 15% to $68 billion. The European Union grew 18% to $455 billion, contributing the largest share to the global increase. US investment rose 3.5% to $378 billion, despite federal policy headwinds.

Clean energy supply chain investment, including new clean-tech manufacturing facilities and battery metals production assets, grew 6% to $127 billion in 2025. This reflects factories commissioned for solar, battery, electrolyzer and wind equipment, along with mines and processing facilities for battery metals. Growth was driven largely by battery manufacturing and materials investment. Overcapacity continues to affect supply chain sectors, placing downward pressure on clean-tech product prices. China remains the dominant market for supply chain investment and is expected to maintain that position over the next several years.

Climate-tech companies raised $77.3 billion in private and public equity in 2025, up 53% year over year and marking the first annual increase after three consecutive years of decline. Funding growth was led by clean power, energy storage and low-carbon transport companies. Public equity activity rebounded, supported by multibillion-dollar deals in Asia, while venture funding declined for the third consecutive year. Mergers and acquisitions activity remained strong, totaling $99.1 billion in closed deals, a 37% increase from 2024, driven in part by acquisitions in clean power and building sectors tied to global data center expansion.

Energy transition debt issuance reached $1.2 trillion in 2025, up 17% from the prior year. Growth in corporate and project finance flows, each rising 20%, offset a decline in government debt sales as labeled issuances were reduced in more mature transition sectors such as renewables.

Additional findings from the 2026 report indicate that data center investment reached approximately $500 billion in 2025, exceeding solar investment but remaining below electrified transport in scale. Established sectors including renewables, storage, electric vehicles and grids continue to dominate overall spending. While China’s leadership in clean-tech manufacturing investment remains significant, its share of annual investment is gradually declining as the US, EU and India expand domestic supply chains. Supply chain investment is expected to continue growing faster than spending required under BNEF’s Economic Transition Scenario, though wind manufacturing may lag. Maintaining alignment with net-zero pathways will require a significant increase in wind manufacturing investment, while projected battery metals additions could result in long-term misalignment if expansion slows as currently anticipated.

The full report, including a data viewer, country-level analysis and a semi-annual renewables deep dive, is available to clients on bnef.com and the Bloomberg Terminal. A public summary version is also available.

EVinfo.net’s Take: EVs and Clean Energy Will Keep Growing in the USA and Worldwide

The global energy transition is no longer a speculative trend. It is a structural shift in capital allocation, industrial policy, and consumer behavior. In the United States and worldwide, electric vehicles and clean energy technologies continue to scale, even amid policy uncertainty and macroeconomic volatility.

In the United States, EV adoption continues to expand as automakers diversify model offerings across price points and segments. Battery costs have declined over the past decade, charging networks are expanding along highways and in urban centers, and utilities are modernizing distribution systems to accommodate higher electrification loads. Even as federal policies fluctuate, state-level mandates, zero-emission vehicle standards, and utility investment frameworks provide structural support for continued deployment.

Globally, China remains the largest clean-tech manufacturing hub, but investment is increasingly distributed across the U.S., the European Union, and India as governments prioritize domestic supply chains. Renewable energy and energy storage have become mainstream infrastructure assets, supported by mature financing models and improving project economics. Grid investment, in particular, is accelerating as countries respond to rising electricity demand from electrified transport, heat pumps, and large data center buildouts.

Corporate capital markets activity reinforces this trajectory. Climate-tech equity fundraising rebounded in 2025, and energy transition debt issuance surpassed $1 trillion. Institutional investors, infrastructure funds, and sovereign entities are treating clean energy as core allocation rather than niche exposure.

Importantly, the expansion of EVs and renewables is increasingly driven by economics rather than incentives alone. In many regions, new solar and wind generation are cost-competitive with fossil alternatives. Total cost of ownership for electric vehicles continues to improve, particularly for high-utilization fleets. These fundamentals create resilience against short-term policy swings.

The path forward will require continued grid modernization, transmission expansion, critical mineral supply development, and manufacturing scale-up. However, the direction of travel is clear. Electrification is becoming the default pathway for transportation and power systems.

EVs and clean energy are not peaking. They are compounding. In the U.S. and worldwide, the energy transition remains one of the defining industrial expansions of the 21st century.

Electric Vehicle Marketing Consultant, Writer and Editor. Publisher EVinfo.net.

Services