The U.S. Got Over 3,000 New Fast Charging Plugs In Q1 2026, Uptime Increasing

The U.S. market for new electric vehicles is not experiencing strong growth at the moment, but that has not slowed the pace of expansion among EV charging providers. Companies across the sector continue to build out infrastructure, maintaining momentum despite softer vehicle sales.

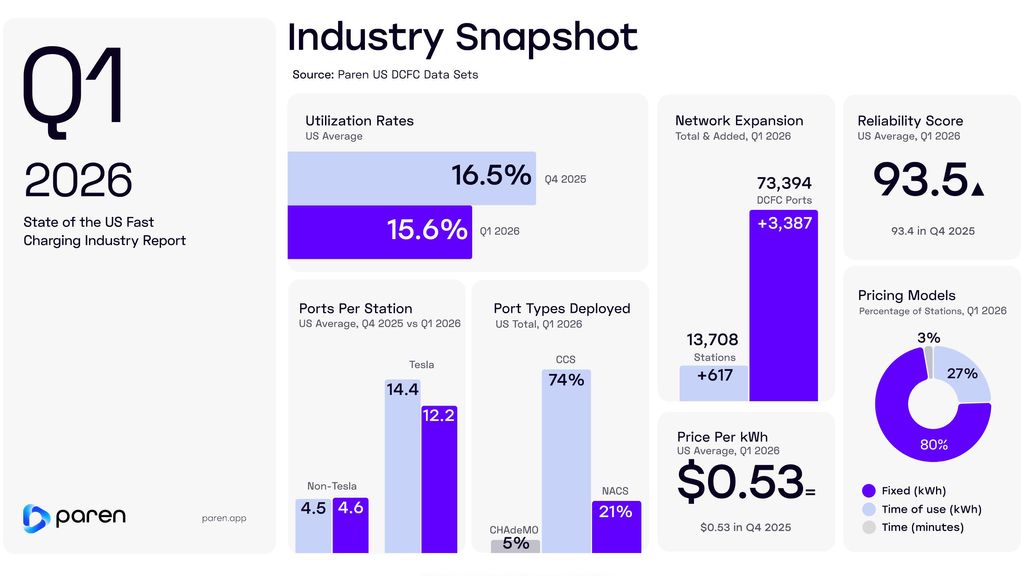

In the first quarter alone, more than 3,000 new DC fast charging plugs were added nationwide, based on data from Paren, a platform that monitors over 95% of the country’s fast-charging network in real time. From January through March, operators deployed 3,387 new ports and brought 617 new stations online. This pushed the national total to 13,708 stations and 73,394 ports. The pace of growth closely mirrors the first quarter of last year, when 3,331 ports were installed, indicating that expansion has remained consistent year over year. Utilization rates have also held steady, signaling that demand continues to absorb the added capacity.

At the same time, the strategy behind network expansion is shifting in 2026. Rather than focusing primarily on building entirely new sites, charging companies are increasingly concentrating on expanding existing locations by adding more stalls. This approach allows operators to scale capacity more efficiently at proven sites. In parallel, most new installations are high-power chargers, with the majority delivering more than 250 kilowatts, reflecting a broader move toward faster charging performance.

Reliability is also improving as operators incorporate lessons from earlier deployments. Average uptime across networks has increased to between 90% and 95%, compared to a range of roughly 85% to 92% last year. Pricing, meanwhile, has remained relatively stable, with most stations charging between $0.45 and $0.55 per kilowatt-hour, even as fuel prices remain elevated and continue to draw attention to charging costs.

Tesla remains the largest player in the U.S. DC fast charging market, though its share of new installations has declined. The company added 880 ports in the first quarter, representing 26% of total deployments, down from levels exceeding 40% in prior periods. Other operators are expanding their presence, with Ionna installing 278 ports and Red E adding 264.

Connector preferences continue to be led by CCS1, while Tesla’s NACS standard is gaining traction. During the quarter, non-Tesla networks deployed 2,102 CCS1 connectors alongside 606 NACS ports. Meanwhile, 154 CHAdeMO ports were added, a legacy standard once used by earlier models such as the Nissan Leaf but now largely phased out. Despite this shift, non-Tesla sites still maintain more CHAdeMO connectors than NACS, even as vehicles equipped with NACS continue to increase in number.

EV sales declined by 27% in the first quarter compared to the same period last year, yet charging companies are continuing to invest. Infrastructure projects often require long planning and construction timelines, limiting the ability to adjust quickly to short-term market fluctuations. At the same time, there remains a clear need to support the growing number of EVs already in operation, as well as those entering the market. Over the longer term, operators are positioning themselves for inevitable renewed growth in EV adoption by ensuring charging capacity is in place ahead of demand.